INFLATION BREAKEVENS AS A SIGNAL

INFLATION BREAKEVENS AS A SIGNAL

Why the 'tourist is watching these indicators like a hawk

I promised another post on inflation breakevens, and although over the years I have written about this topic probably too often, I am taking another shot at it because it’s that important.

Inflation breakevens sound complicated, but in reality, they are quite simple.

Most developed-economy governments offer both nominal and inflation protected bonds. Nominal bonds are the type most people know. They pay a fixed rate of interest and neither the coupon nor the maturity change. As interest rates fluctuate, the price of the bond changes to reflect the higher or lower yields. For example, if the government issues a 10-year bond with a yield of 3.25% and market rates fall to 2.50%, the price of this issue will rise to reflect the lower yield. Plenty of hedge funds, banks and other market participants actively arbitrage the different bonds, attempting to earn attractive risk-adjusted returns by buying and selling mispriced individual issues. It’s a liquid, actively traded market and on the whole, largely quite efficient.

There is another type of bonds called inflation protected securities. In the US, we know them as TIPS (Treasury Inflation Protected Securities), but in most other countries, you will hear them referred to as real-return bonds.

These bonds have little quirks, but their main commonality is that they offer a coupon yield (just like nominal bonds), but on top of that, also return to the holder the level of inflation over the life of the bond.

Let’s assume an investor buys a 10-year TIPS note with a yield of 0.75%, the actual return will be 0.75% each year plus whatever inflation ends up averaging over this period. If the Federal Reserve manages to hit their inflation target square on the head at 2%, this investor will earn 2.75% over the life of the note.

Now, let’s imagine this same investor could have instead bought a 10-year nominal note with a yield of 3.25%. Obviously, this would have proven to be a better investment, as that yield (3.25%) is higher than the achieved yield (2.75%), on the TIPS note.

However, at the time, it was difficult to know where inflation would average over the next decade.

Inflation breakevens are simply the difference between this nominal note yield and the TIPS note yield.

Inflation breakevens represent the future level of inflation at which investors are indifferent to either type of note.

Doesn’t seem that hard after all, does it?

Sometimes it can seem a little more complicated because TIPS are trading at a negative yield.

In my example above, I chose a TIP with a positive real yield. That means that the investor will earn a positive return on top of inflation.

Well, unfortunately that’s no longer the case.

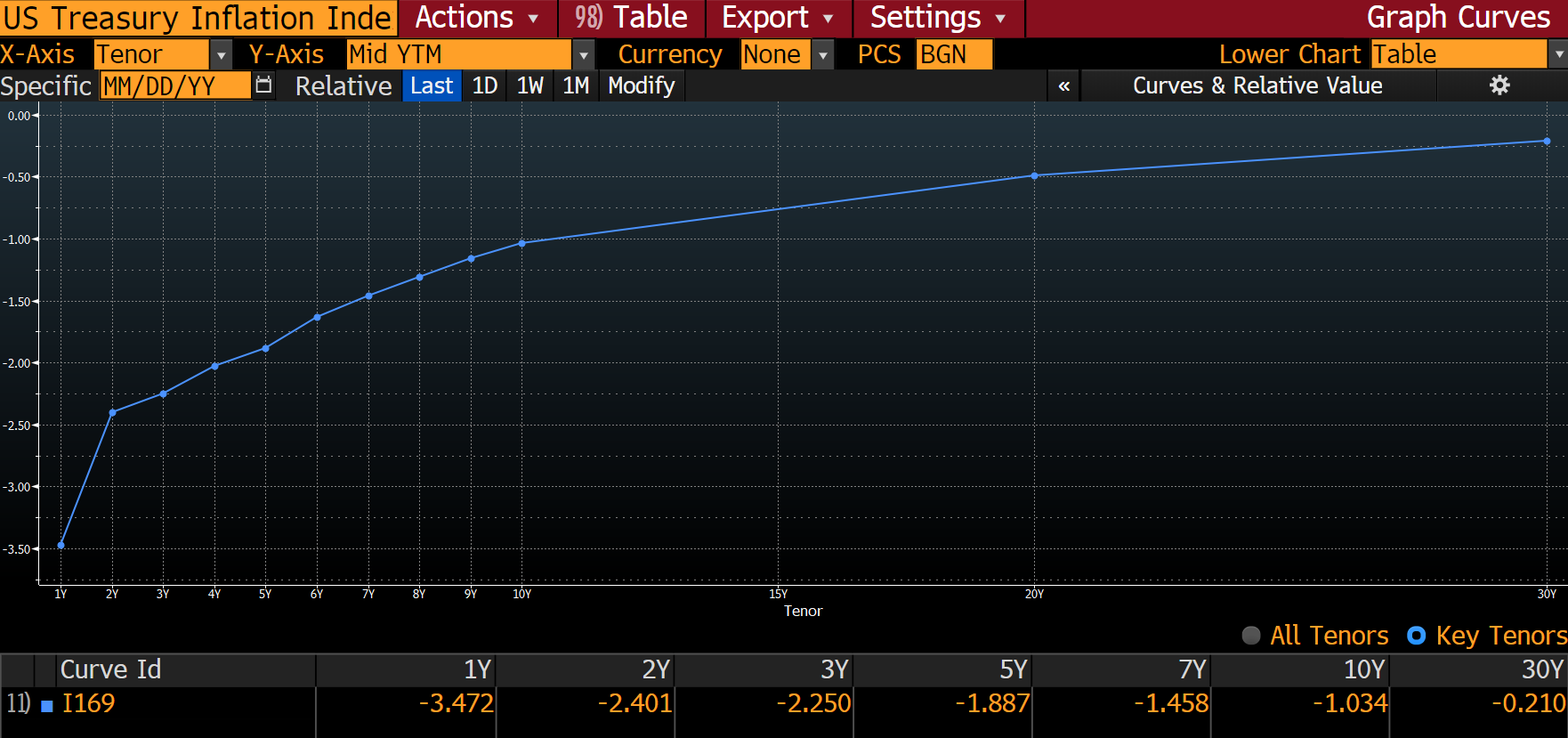

Today, the entire TIPS curve trades at a negative yield.

This means that no matter how far you go out the curve, you will not earn a rate higher than inflation over the life of the TIPS fixed-income instrument.

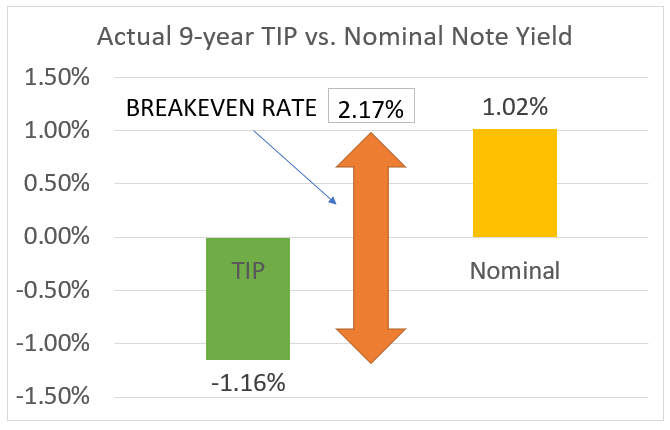

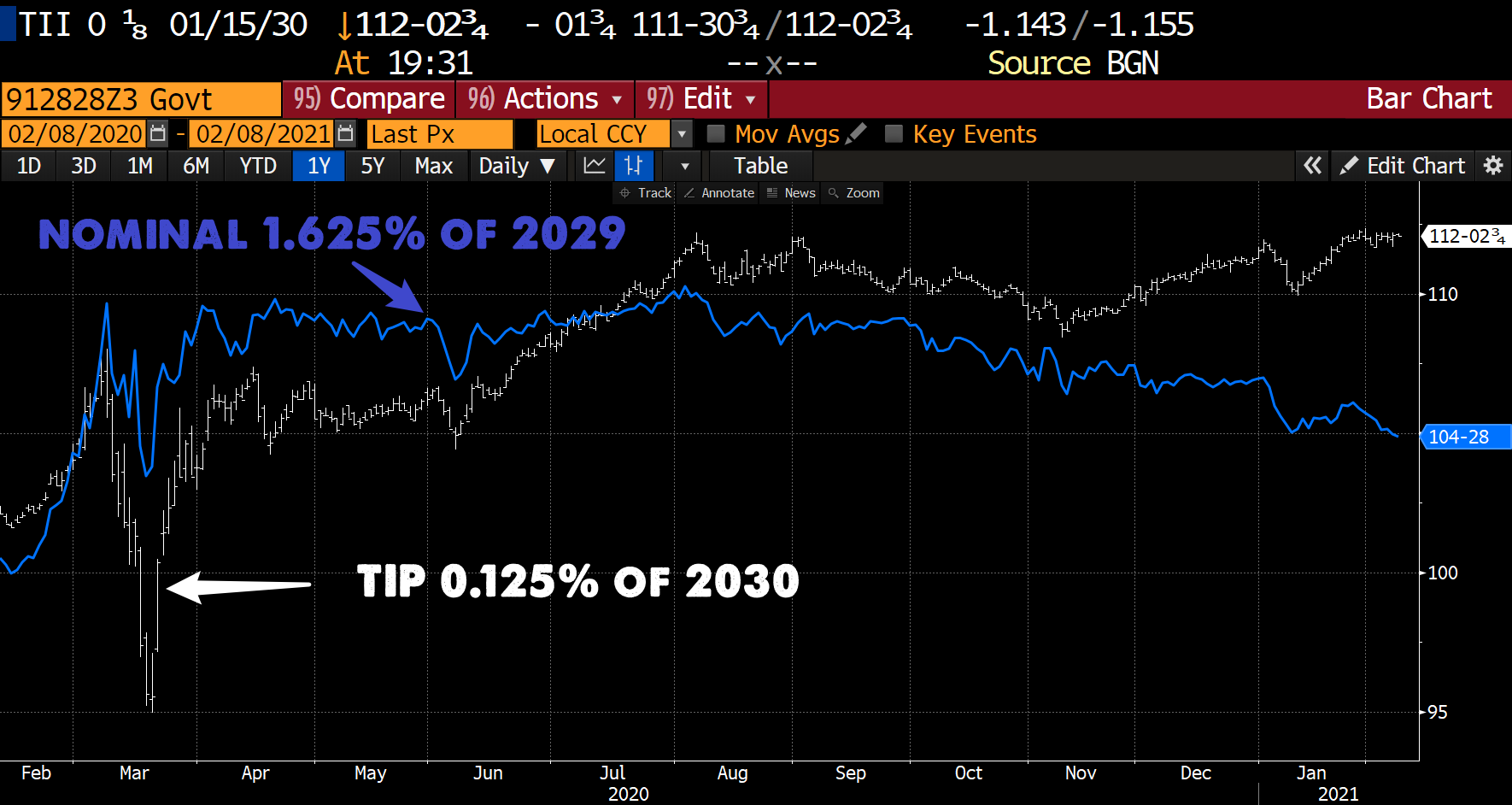

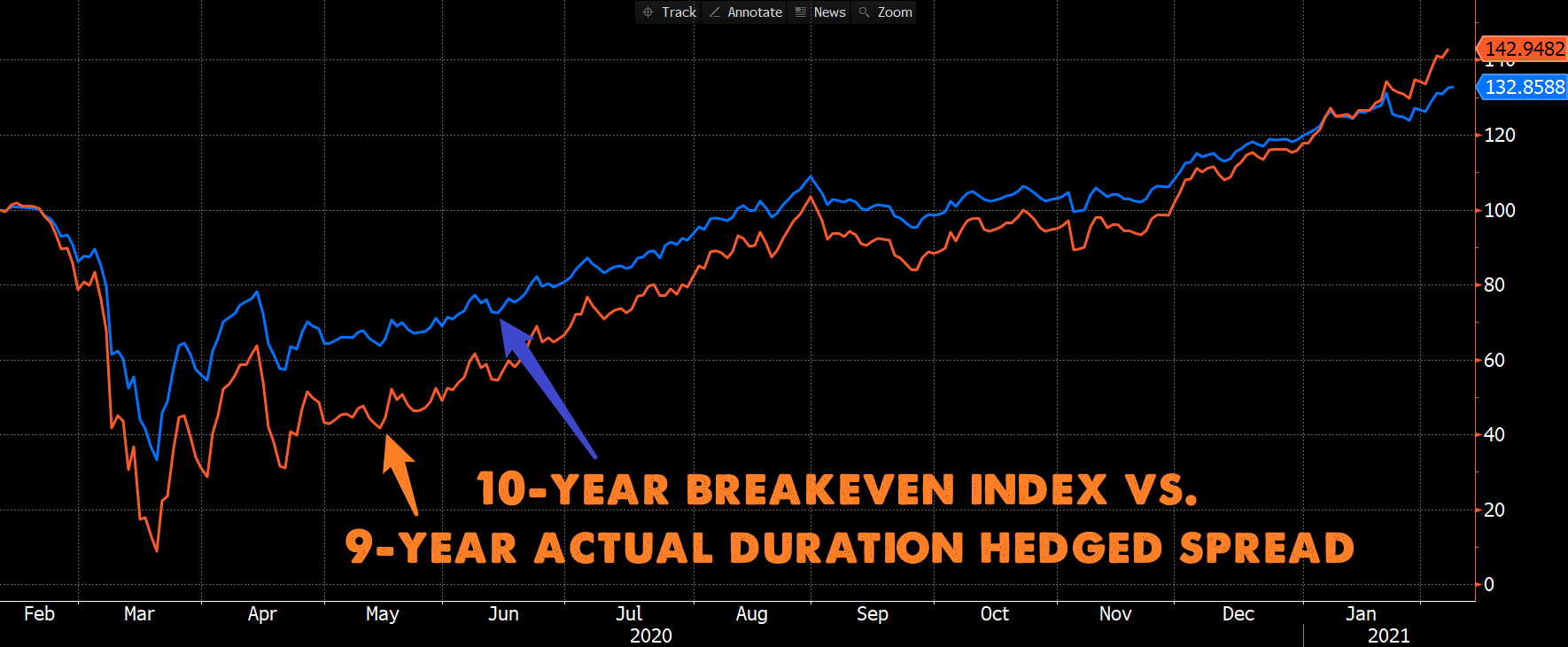

I have constructed a new graph with the current actual 9-year TIPS (the 1/8s of 01/15/2030) and nominal note (1 5/8s of 08/15/2029) yields. I used the 9-year tenor because I want to show the price action in these securities over the past year, so I needed to use last year’s 10-year issuance.

The graph is slightly different because the end point for the TIPS’ yield is below zero, so now the BREAKEVEN RATE is the point from the bottom of the green bar to the top of the yellow bar.

The 9-year TIP yield is negative 1.16% while the 9-year nominal note is 1.02%. This gives us a breakeven of 2.18% (it rounded differently on my graph above).

What does this mean in the real world?

While nominal note investors will earn a positive return of a little over 1%, they should expect to lose over 1% in real terms - that is the return after inflation. The market is expecting an inflation rate of 2.18% over the life of the notes.

Think about inflation breakevens as the clearing price of the market’s willingness to hold TIPS over nominal notes. When the market expects higher future inflation, they are more willing to bid up TIPS. When inflation is expected to be more muted, participants pay more for nominal notes (on a relative basis).

So, when I say that I want to be long inflation inflation breakevens, that means I expect the relative price of TIPS to move higher versus the nominal notes.

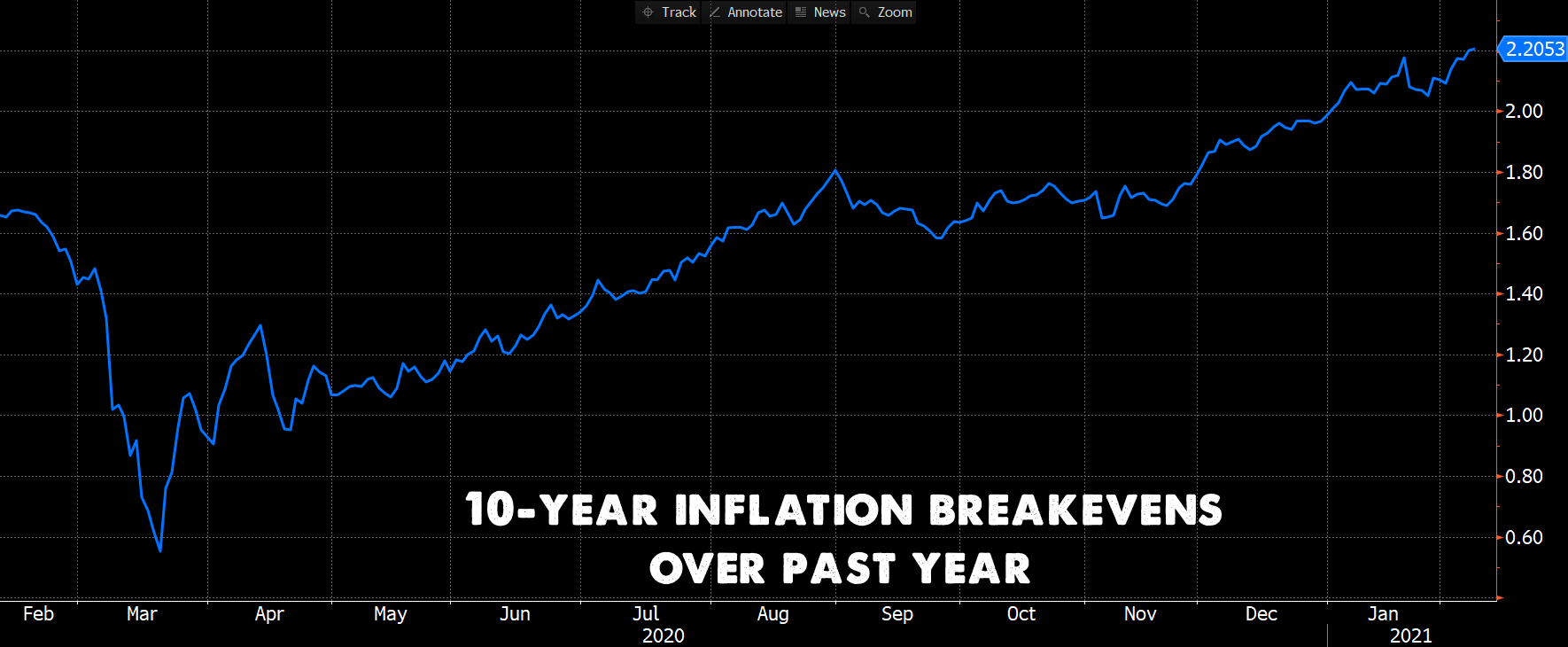

And what have these inflation breakevens done over the past year?

Well, after plummeting during the COVID crisis, inflation breakevens have been steadily marching higher. Recently, much of the inflation breakeven curve broke out to new highs for this move.

But how does this relate back to our different 9-year notes?

I chose two issues with relatively close durations so that you could see the contrasting performance over the past year.

The white bar is the TIP. You can see that during the COVID crisis, it suffered much worse and underperformed dramatically. Investors did not want to own TIPS during this period as there was little worry about future inflation. In fact, more were worried about deflation, so they sold the TIPS aggressively versus nominal bonds.

However, you might notice that, since July, the nominal bond (blue line) has been sinking, while the TIPS issue has been rallying.

If we duration match these two bonds (adjust them for the slight difference in sensitivity to interest rate changes), then we can come up with the actual 9-year relative performance spread of inflation-protected-notes versus nominal.

Adding that real-world 9-year spread to the previous 10-year inflation breakeven chart, it’s easier to understand what we are looking at when we plot inflation breakevens.

The blue line is the Bloomberg 10-year inflation breakeven index and the orange line is the P&L associated with the 9-year inflation breakeven spread trade.

When it comes to implementing this trade, I don’t bother with the hassles of shorting individual government issues. Instead, I use Treasury note futures. In this case, the Ultra-10-year future offers the best fit.

With the help of a little math, we calculate that we need to buy $150,000 face of the TIPS issue of 1/8s of 01/15/30 per March 2021 Ultra-10-year-note future (symbol UXY in the Bloomberg - TN in IB).

I created the P&L associated with this trade. I indexed it to 100, starting a year ago.

This P&L assumes no leverage.

So, if you had invested $100 on Feb 8th, 2020, you would have seen it fall 20% in the depths of the COVID crisis, but has since rallied to a 16.5% return.

The reason I like using the actual TIPS and the treasury futures as opposed to other instruments like RINF? I can customize the tenor of my trade. Although I have used a 9-year TIP, most of my positions are 25+ years in length. But even more importantly, because these are government fixed-income securities, most brokers offer considerable leverage on the positions.

For example, on the long TIPS side, Interactive Brokers makes me put up 6.4% of the notional amount for that 2029 issue. The bid offer on the notes is $0.06 wide and currently quoted 2MM by 6MM. More than enough liquidity for an odd-lotter like me. On the short side, the margin is around 1% for the treasury future, so on the whole, I can carry this trade for 7.5% of notional.

Now, there is no way I would use the full amount of leverage offered to me by the brokers. During COVID, this trade marked down 20%, so you need to take into account the potential loss on any drawdowns when determining position size.

But, I run a highly levered book with many different trades. This includes outright directional trades, but also arbs. So, for me, trading inflation breakevens through the underlying TIPS issues makes much more sense. It keeps my options open for when other opportunities come along.

Right now, inflation breakevens represent 30% of my book and I consider them a core holding.

REFLATION versus INFLATION re-visited

Over the past year, the Federal Reserve has purchased more TIPS than during any other time in history. But - they also purchased more of ABSOLUTELY EVERYTHING!

The reason I bring this up? There is a group of hard-money-strategists who love shouting at the top of their lungs how the Federal Reserve is manipulating breakeven expectations by transacting in the TIPS market.

Is the Federal Reserve influencing breakeven rates? Probably a little. What part of the fixed-income market did they not bully around last year?

But here is the 10-year inflation swap overlayed on the 10-year breakeven rate:

If the Fed was unduly influencing the TIPS market, you would have seen these two series diverge.

When you hear commentators preaching how inflation expectations are simply the result of the Fed buying TIPS, ignore them.

However, that doesn’t mean inflation breakevens aren’t moving because of the “reflation” that I mentioned in my piece the other day [WHEN REFLATION BECOMES INFLATION]. The investing world is embracing the “REFLATION” trade, and there is no doubt - that includes inflation breakevens!

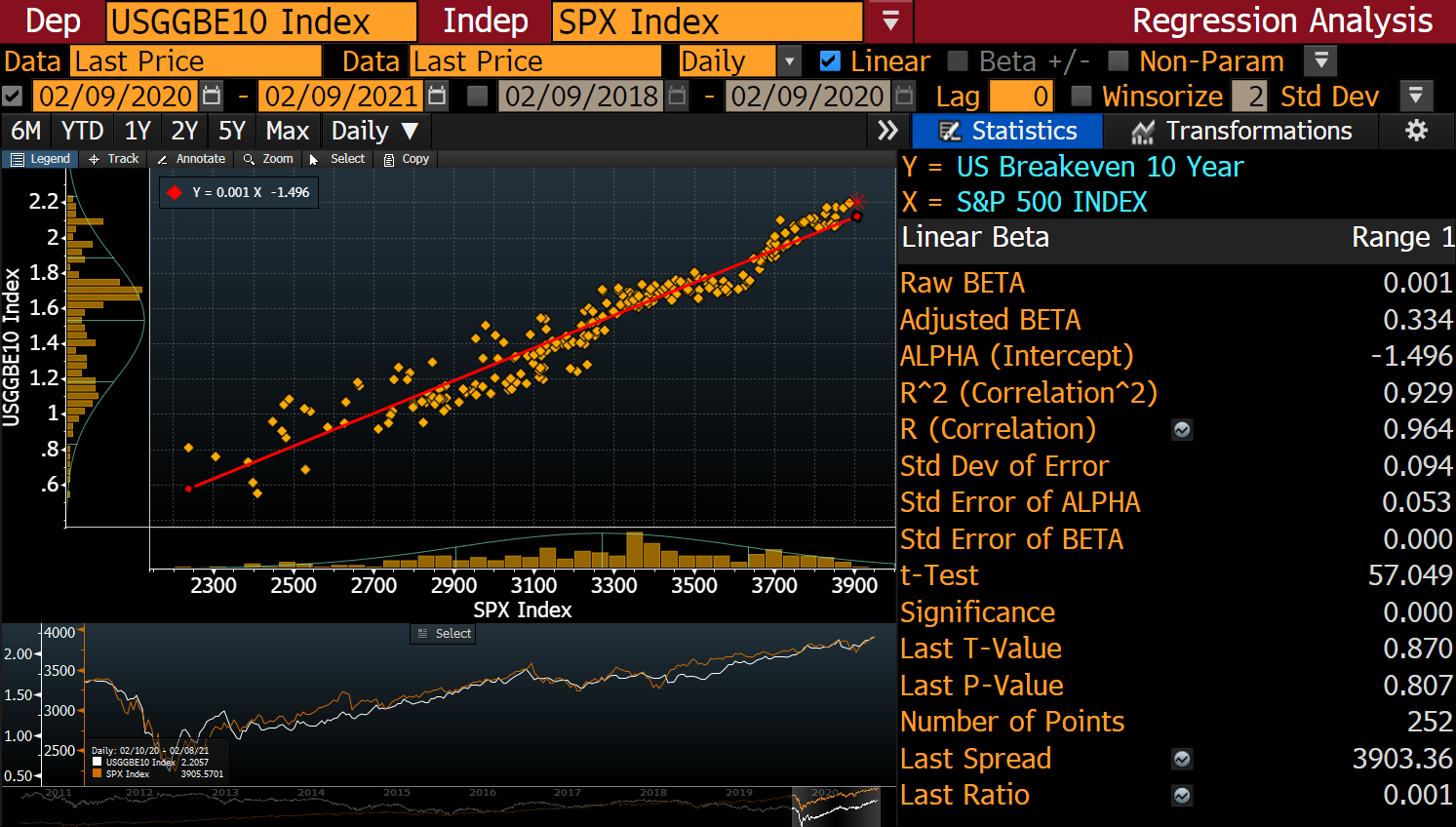

Therefore, when a well-respected macro shop recently wrote a piece warning “DON’T BE FOOLED BY WHAT’S HAPPENING WITH BREAKEVEN RATES”, I sat up and took notice.

Their argument was that TIPS liquidity premiums are simply moving in lockstep with stock prices. The COVID-crisis saw investors abandon the riskiest of securities (which include TIPS), and the relative outperformance of the past nine-months has simply been the result of the Fed pushing liquidity back into the financial system.

Here is the same 10-year inflation breakeven (white bar) with the S&P 500 included (blue line):

Yup. The macro shop are spot-on. It’s all one big trade.

Take a gander at this regression analysis of the 10-year breakeven versus the S&P 500 over the past year to get a sense of how closely they are trading together.

And that was my point with the REFLATION versus INFLATION piece.

So far, we’ve only experienced REFLATION. No doubt about it.

However, the next stage - when INFLATION takes the leadership baton from REFLATION - will see a change in relationships like “inflation breakevens versus stocks”.

During the REFLATION phase, you could have been long inflation breakevens, or you could have been long stocks. It didn’t matter. During the INFLATION phase, inflation breakevens will vastly outperform stocks on a risk-adjusted basis.

When people ask why I am so enamoured with inflation breakevens, it’s because inflation breakevens will win in either environment.

I will be coming back to this regression analysis in the future. It will be one of my main clues that we have shifted from REFLATION to INFLATION. Keep your eyes peeled.

Thanks for reading,

Kevin Muir

the MacroTourist

Great piece Kev

Totally off-topic, but do you have any idea what is going on with smallcaps? Is TF just going to go up 2%/day perpetually now? Index is up 50% since November, just breathtaking.